Budgeting Tips for Couples

Money can be a major source of conflict for many couples. Differing attitudes about spending, saving, and finances in general can create tension and disagreements in a relationship. Fortunately, with some planning, communication, and compromise, couples can create a budget that works for both partners. Establishing financial compatibility is an important component of a healthy long-lasting relationship.

In this blog article, we will provide you useful advice for couples looking to manage their money successfully together. It covers key topics like identifying shared financial goals, creating a system for tracking expenses, dividing financial responsibilities, sticking to your budget, talking openly about money, getting on the same page about spending habits, saving and investing as a team, dealing with debt, and adjusting your budget over time. With these tips for budgeting as a couple, you can build unity around your finances.

Discuss Your Financial Values and Priorities

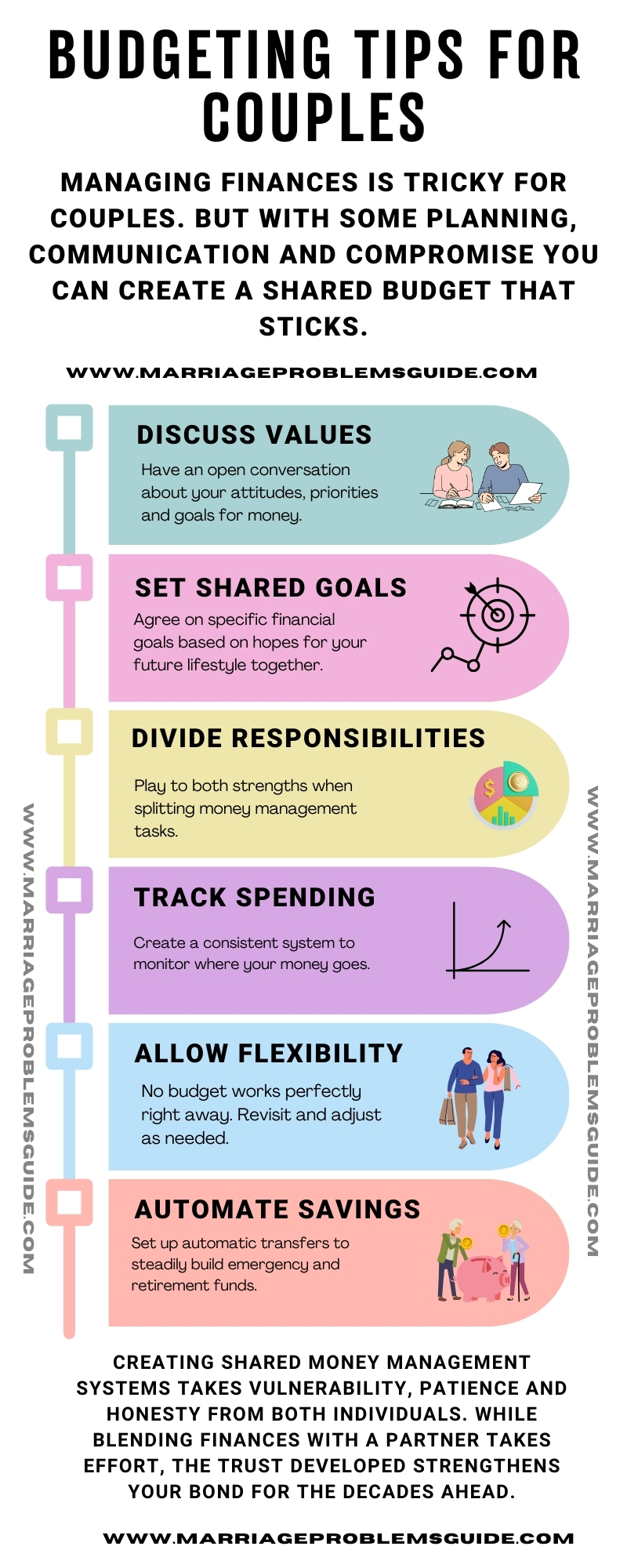

A budgets begins not with dollar amounts, but with an honest conversation. Sit down together and talk about your underlying beliefs, priorities and values when it comes to money. Getting these out in the open is key to understanding each other’s point of view when it comes to your finances.

Some key questions to ask each other:

- What did you learn about money growing up?

- What does money represent for you and what emotions does it trigger?

- What are your short and long term saving goals? Retirement plans?

- Do you have certain spending rules or restrictions you’d like to implement?

- What problems do you foresee around our money management as a couple?

Identifying these values upfront makes it easier to come to agreements about your shared budget. Compromise is essential, so approach this conversation openly and without judgement. The goal is to find your overlapping money values.

Agree On Shared Financial Goals

Now that your money values are out in the open, it’s time to talk specifics when it comes to financial goals. As a couple, sit down and ask where you want your money to go and what matters most. Get detailed about what lifestyle you want now and years down the road.

Some shared goals may include:

- Saving up for a dream vacation abroad

- Paying off student loan or credit card debt

- Joining finances to buy a house one day

- Starting a wedding or emergency fund

- Paying for continuing education

- Saving for retirement to start travel later in life

Whatever your budgeting priorities as a couple, write them down together. This keeps you focused on what matters most as you make spending decisions going forward. Revisit these goals periodically to check-in and update as needed.

Create System for Tracking Expenses

Now here comes the fun part – tracking what actually gets spent! Begin documenting your individual expenses as well as those you share. This gives you awareness into spending patterns and cash flow.

Approach this as a team effort by adopting a shared expense tracking method. Some options include:

- Shared app or budgeting software: User-friendly apps like Honeydue, Zeta, or You Need a Budget provide a centralized place for couples to add expenses, set budgets, save towards goals and analyze monthly cash flow.

- Spreadsheets: Create different tabs for joint expenses like rent, household items, utilities and individual tabs for your own day-to-day spending on things like coffee, clothes or hobbies.

- Receipt Collection: Have an envelope or bin where you deposit receipts. Set time weekly or monthly to categorize expenses for better spending awareness.

No matter what system you choose, consistency is key when tracking expenses. Set reminders to keep each other accountable.

Divide & Conquer with Financial Responsibilities

One secret for harmonious budgeting? Divide and conquer key money tasks based on each person’s strengths. Play to both yours and your partner’s abilities.

Split essential responsibilities like:

- Handling bills and payments: One partner may love automating things while the other prefers manual payments. Alternate months or assign different bills to each person.

- Monitoring spending: One of you may enjoy regularly assessing cash flow using your tracking system while the other schedules occasional budget check-in meetings.

- Researching purchases and deals: Take turns being the lead bargain hunter for big purchases or household necessities.

- Managing accounts and investments: One partner may have the financial know-how to oversee retirement accounts, college savings plans or optimizing interest rates.

Coming together to make major decisions while allowing each individual to own domain over certain tasks makes money management far less overwhelming.

Set Mutual Guidelines Within Your Budget

Now take everything you’ve discussed – your goals, spending habits and responsibilities – and funnel it into a shared budget. Outline guidelines you both can live with when it comes spending.

Some categories to include:

1. Housing – outline monthly rent/mortgage, utilities, maintenance costs

2. Transportation – car payments, fuel, insurance and registration fees

3. Food – groceries, restaurants, meal kits or takeout

4. Personal – individual clothing, self-care or hobby purchases

5. Discretionary – date nights, travel, concerts, gifts or donations

6. Financial – debt payments, banking fees, financial advising

7. Savings – emergency fund contributions, retirement, education

Set limits that align with the percentages you want directed towards needs vs wants each month. Allow for flexibility – no budget is perfect right away. You want room to make mistakes and adjust. Automate saving and bill payments when possible.

Use your system for tracking real spending and check in monthly to address any areas where you went over budget. Should additional expenses pop up, have an agreement in place for discussing unplanned spending above a set $ amount.

Utilize Online Budgeting Tools

While you can create a custom budget from scratch, it helps to have an initial framework. Sign up for a user-friendly budgeting app or visit a bank website for money management guidance.

Web tools provide:

- Customizable budget templates covering typical households costs

- Pie charts and graphs visualizing spending breakdowns

- Calculators offering specific saving targets for goals like a getting out debt, buying a car or affording college

- Categories with average expenditure amounts based on factors like income level and family size

- Educational resources outlining fundamentals of budgeting

Use these digital tools as a starting point for building mutual guidelines tailored to your individual circumstances as couple.

Have Regular Budgeting Meetings

Congratulations – you’ve made a budget plan! But your money work doesn’t stop here. Consistency is crucial when learning how to successfully budget together. Sit down once a month for regular check-ins:

- Compare planned budgets vs actual spending using your tracking system

- Discuss when and why you went over budget in any areas

- Hold each other accountable rather than assign blame

- Renegotiate categories to increase realism and flexibility

- Check progress made towards current financial goals

- Address any upcoming expenses and stay a step ahead

Building this habit keeps your budget top of mind. It provides space to communicate about money goals without frustration boiling over after the fact. Make it fun by alternating who hosts – cook a nice meal or go out for coffee or dessert!

Talk Openly About Spending Habits

Managing money together shines a spotlight on individual spending styles. Be honest with your partner about tendencies that may contribute to overspending:

1. Impulse buying – Are you a sucker for in-the-moment purchases without second thought?

2. Convenience bias – Will extra energy to compare prices when shopping?

3. Present bias – Do you opt for instant gratification with purchases vs thinking long term?

4. Lifestyle inflation creep – Have your tastes and spending habits gotten pricier over time?

By pinpointing potential pitfalls you can then problem solve together. Create “cool down” periods for bigger purchases. Institute store “wait lists” when temptation strikes impulse shoppers. Automate bigger chunks towards savings goals before free cash gets spent first.

Non-judgmentally analyzing habits prevents assumptions. And it leads to unified solutions.

Agree On Approaches to Variable/Unexpected Costs

No budget anticipates each surprise expense. The heating system fails mid-winter or the car needs a repair. Your company lays people off. A global pandemic halts travel plans.

Life provides plenty of financial shocks. These unpredictable hits can tank a couple’s budget – fast. Unless you plan ahead for how to handle them together. Some key ground rules to set:

1. Emergency Fund

Automatically direct a portion of each paycheck into a shared savings account. Grow this to cover 3-6 months’ expenses. That way when crisis hits, cash gets pulled from savings vs sinking you further in debt using credit cards or loans.

2. Job Loss

Draft an action plan that kicks in should one partner face unemployment. Detail how to reduce spending, temporarily reallocate bill responsibilities, and dip into emergency reserves or other assets if needed.

3. Irregular Windfalls

Decide rules upfront for any workplace bonuses or inheritance money. Do certain percentages automatically go towards debt or savings versus fun extras?

Your agreements mean no fighting when surprises inevitably occur. Preparation eases the sting when life throws budget bombshells.

Automate Saving and Investing

Retirement and other financial goals creep closer day by day. But the present feels far more tangible than the future. That’s why psychology shows we often prioritize current wants over long-term needs – no matter how much our future selves beg us to save!

Outsmart this bias as a couple by setting up automatic contributions that quietly build your savings behind the scenes:

1. Retirement Accounts

Have percentages from each paycheck automatically invested into IRAs, 401(k)s or other tax-advantaged retirement plans. Slow and steady compounding growth adds up.

2. Emergency Fund

Use auto-deposits to steadily feed your cash reserves for life surprises discussed earlier.

3. College Saving

If kids may factor into your future, start gently contributing to 529 plans each month.

4. General Goals

Pick a certain financial milestone like saving for a home, trip or to start a business one day and automatically allocate funds each month.

Dig into investing together by chatting about risk tolerance and researching different account types. Over time build a nest egg that turns future financial goals into realities.

Work Together to Pay Off Debt

Debt drains budgets and adds stress that permeates relationships in subtle ways. Come clean with your partner by sharing any outstanding balances – credit card bills, student loans, personal debts to family and the like.

With all owed amounts visible, make an attack plan:

- List debts from highest to lowest interest rates – focusing first on most costly balances saves money long run

- Avalanche Method: Put any extra cash each month towards highest interest debt while making minimums on the rest

- Snowball Method: Pay minimums on all debts, then aggressively apply extra payments only towards smallest balance. Seeing debts get paid off keeps you motivated!

Once you wipe current debts, commit as a couple to discuss any major future loans. Set guidelines regarding appropriate levels of borrowing aligning with budget priorities.

Getting aligned on past and future debt helps couples build assets rather than over-rely on expensive credit.

Check-In and Adjust Your Budget

Building a budget is rarely “one and done.” As life progresses, check-in to realign your plan. Scheduling periodic money reviews encourages flexibility that maintains harmony.

Check-in when:

Incomes change: Promotions, job transitions or salary cuts alter cash flow available

Major goals get met: Reaching a savings milestone or finally paying off debts frees up future dollars

Responsibilities expand: Buying a house, having kids, caring for parents – budget for new priorities

Values shift: A partner discovers FIRE retirement ambitions or sets sights on a new career

Make course corrections together without feelings of failure. Adaptability keeps couples budgeting – not each person guarding their own monetary preferences.

Money goals and habits will transform over months and years. But honest conversations ensure continued unity that weathers any storm.

Conclusion

Creating shared money management systems takes vulnerability, patience, and honesty from both individuals. While blending finances with a partner takes effort, the trust developed strengthens your bond for the decades ahead.